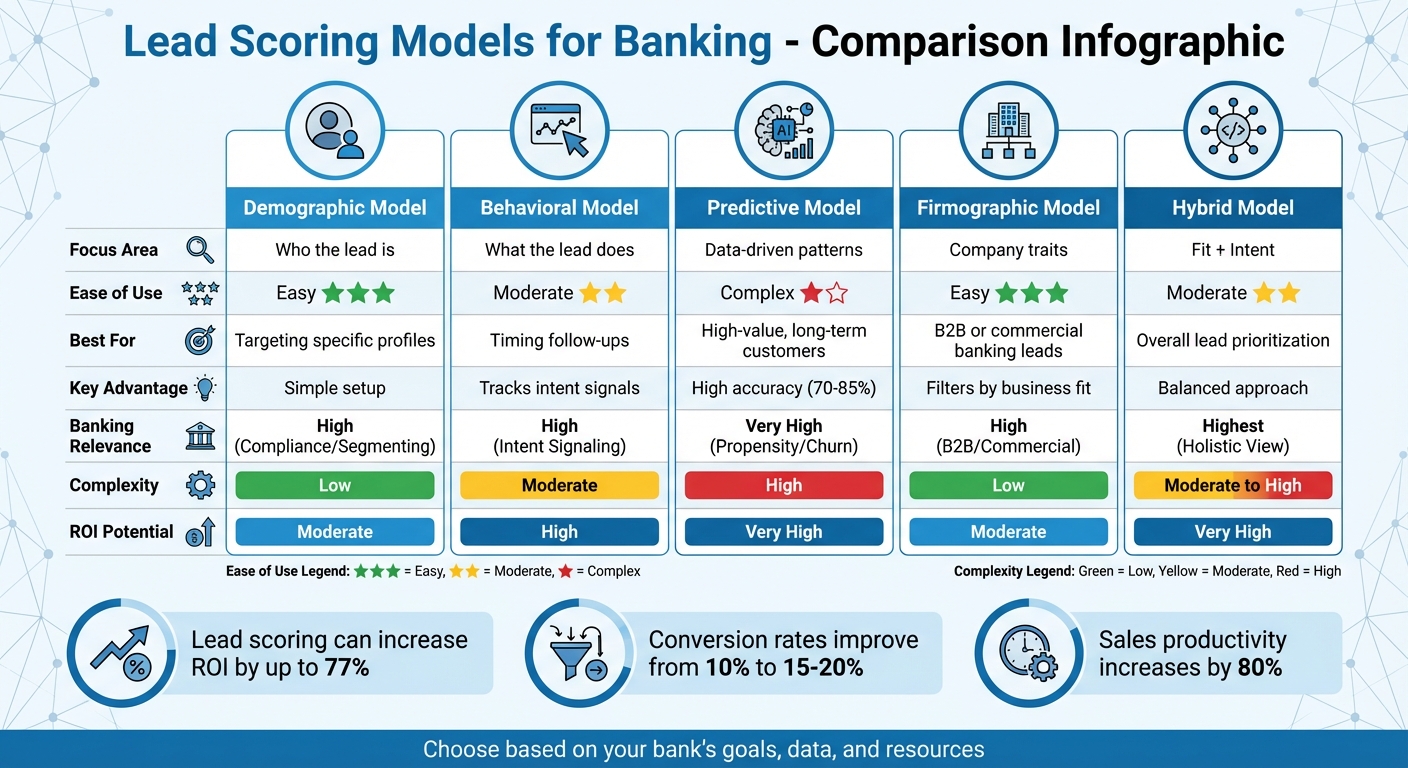

5 Lead Scoring Models for Banking Success

March 26, 2026In banking, not all leads are created equal. Lead scoring helps prioritize prospects by assigning a score based on their potential to convert. This article outlines five lead scoring models tailored for banking:

- Demographic Model: Focuses on who the lead is (e.g., income, job title, location). Simple to implement and ideal for targeting specific customer profiles.

- Behavioral Model: Tracks actions like website visits or email clicks to gauge intent. Great for identifying when a lead is ready to act.

- Predictive Model: Uses AI to analyze patterns and predict conversion likelihood. Offers high accuracy but requires more data and setup effort.

- Firmographic Model: Evaluates company-level traits like size, revenue, and industry. Best for B2B or commercial banking.

- Hybrid Model: Combines demographic and behavioral data for a complete view. Balances fit and intent, making it the most effective overall.

Quick Comparison

| Model Type | Focus Area | Ease of Use | Best For | Key Advantage |

|---|---|---|---|---|

| Demographic | Who the lead is | Easy | Targeting specific profiles | Simple setup |

| Behavioral | What the lead does | Moderate | Timing follow-ups | Tracks intent signals |

| Predictive | Data-driven patterns | Complex | High-value, long-term customers | High accuracy |

| Firmographic | Company traits | Easy | B2B or commercial banking leads | Filters by business fit |

| Hybrid | Fit + Intent | Moderate | Overall lead prioritization | Balanced approach |

Each model serves a unique purpose, so the best choice depends on your bank's goals, data, and resources. Whether you need simplicity or advanced analytics, these models can help maximize conversions and improve sales efficiency.

5 Lead Scoring Models for Banking: Comparison Chart

Using AI for predictive leads scoring in Clay.com

sbb-itb-cef5bf6

1. Demographic Lead Scoring Model

The Demographic Lead Scoring Model focuses on evaluating who a lead is rather than what they do. It assigns points based on specific details like job title, income level, location, age, and company size. This allows banks to identify prospects who closely align with their Ideal Customer Profile (ICP). By using this straightforward method, banks can fine-tune their scoring system to match their unique needs.

Relevance to Banking-Specific Needs

Banks can customize demographic scoring to align with their product offerings. For example:

- A wealth management division might award +25 points to individuals earning over $150,000 annually.

- A student loan team could prioritize the 18–24 age group with a +15 point adjustment.

- Commercial banking might focus on C-level executives (+20 points) or businesses with enterprise-level revenue (+15 points) to zero in on decision-makers who hold purchasing power.

Negative scoring also plays a critical role. Banks may deduct points for leads that are less likely to convert, such as those from unsuitable locations (–10 to –50 points), using personal email domains for business inquiries (–10 points), or operating in restricted industries. This ensures sales teams focus their energy on high-potential prospects.

Ease of Implementation for Financial Institutions

This model is rule-based, making it easy for stakeholders to understand and implement. Banks can start small, focusing on essential variables like location, income, job title, industry, and age - no need for advanced predictive tools.

"Lead scoring is fundamentally math informed by context."

- Colin Price, Head of Growth, NC Squared

The flexibility of this model is a major advantage. For instance, if a bank launches a new mortgage product aimed at first-time homebuyers, it can quickly adjust scoring criteria to prioritize younger leads or specific income brackets. This adaptability supports quick pivots as business strategies shift.

Effectiveness in Improving Lead Prioritization

Demographic scoring helps banks create clear priority levels (e.g., P1, P2, P3) for leads. For example:

- Leads scoring 80–100 points might go directly to senior relationship managers for immediate follow-up.

- Leads scoring 40–60 points might enter a nurturing campaign for further engagement.

One consulting firm using a similar model saw an 18% increase in revenue by focusing on high-priority leads.

Potential ROI and Customer Acquisition Impact

With a well-developed demographic scoring system, organizations have reported conversion rate improvements - from a baseline of 10% to 15–20%. This ensures marketing budgets are spent on prospects who are most likely to convert.

| Demographic Attribute | Example Banking Criteria | Potential Point Value |

|---|---|---|

| Job Title | C-Level Executive / Business Owner | +20 to +25 points |

| Income/Revenue | High Net Worth / Enterprise Revenue | +15 to +20 points |

| Location | Within target branch zip codes | +10 points |

| Industry | Target sector (e.g., Real Estate) | +10 points |

| Email Domain | Personal email (Gmail/Yahoo) | –10 points |

| Role | Student or Job Seeker | –20 points |

2. Behavioral Lead Scoring Model

The Behavioral Lead Scoring Model focuses on tracking what prospects do rather than who they are. It assigns points based on specific actions like using mortgage or HELOC calculators, downloading loan-related guides, clicking on email links, or repeatedly visiting pricing pages. These behaviors act as subtle clues, helping banks understand where a prospect stands in their financial decision-making journey - especially useful when decisions take time.

Relevance to Banking-Specific Needs

This model allows banks to identify high-intent behaviors that suggest a prospect is ready to take action. For instance, someone who uses a mortgage calculator three times in one week is likely much closer to applying than someone casually browsing general finance articles. Similarly, multiple visits to a mortgage rates page within a short period should trigger quick follow-up actions. By grouping leads based on their browsing history, banks can tailor their approach - for example, treating a credit card inquiry differently from a commercial loan request. Matching behaviors to financial intent ensures marketing strategies are more focused and effective.

Negative scoring further sharpens lead prioritization. For example, deducting points for visits to career pages or frequent trips to customer support sections - actions that suggest a lack of readiness for financial products - helps sales teams concentrate on leads with higher potential. Combining this behavioral data with demographic insights creates a solid foundation for more advanced predictive tools.

Ease of Implementation for Financial Institutions

Banks can start by creating simple, rule-based scoring systems. For example:

- +15 points for downloading a retirement planning guide

- +10 points for clicking through an email

- +25 points for scheduling a branch appointment

As the system evolves, banks can add features like score decay, which reduces points for leads that become less engaged over time. This ensures sales teams focus on active prospects. To make the system work, marketing and sales teams must align on what qualifies as a Marketing Qualified Lead (MQL). If sales teams reject too many leads, it’s a sign the criteria need adjustment.

"Lead scoring only works when it's operationalized."

- Colin Price, Head of Growth, NC Squared

Effectiveness in Improving Lead Prioritization

Behavioral scoring is particularly effective for speeding up lead response times. For example, routing a lead to a loan officer within five minutes of high-intent actions - like repeated visits to pricing pages - can boost conversion rates by 20–40%. Assigning higher points to more significant actions, such as completing a mortgage application versus opening an email, further sharpens prioritization. Leads engaging with high-value content, like webinars, often close at a rate of 75%, compared to an average of 50%.

Potential ROI and Customer Acquisition Impact

Lead scoring can deliver impressive results. Companies have reported up to a 70% increase in lead generation ROI, with conversion rates from prospects to qualified leads jumping from 10% to 15–20%. For example, after a merger, healthcare technology firm Tebra implemented a combined scoring and routing system. This resulted in 40% faster response times and a 30% boost in conversion rates.

| Behavior Category | Action | Scoring Impact |

|---|---|---|

| High Intent | Pricing page visits (3+ times/week) | +25 points |

| High Intent | Mortgage/HELOC calculator usage | +20 points |

| Medium Intent | Whitepaper download | +10 points |

| Low Intent | General email open | +5 points |

| Negative | Career page visit | –10 points |

Next, we’ll dive into how predictive models take lead evaluation to the next level.

3. Predictive Lead Scoring Model

The Predictive Lead Scoring Model uses machine learning to sift through vast amounts of data and predict the likelihood of lead conversions. Unlike traditional models that rely on fixed rules based on demographics or behavior, this approach is dynamic. It continuously learns from conversion trends and evaluates factors like credit scores, loan purposes (purchase vs. refinance), property values, debt-to-income ratios, and transaction history to create a well-rounded view of borrower potential. These models update themselves frequently - every 6 to 24 hours - allowing them to adapt as market conditions change.

Relevance to Banking-Specific Needs

Predictive scoring helps banks identify which prospects are most likely to become long-term, profitable customers. By pulling together data from various sources - credit risk analyses, transaction records, and marketing interactions - it creates detailed profiles of potential clients. This enables banks to offer tailored solutions from the first interaction. Instead of gradually cross-selling products, they can bundle services like commercial loans, treasury management, and private banking right from the start. Advanced systems even assign high-value leads to the loan officers most likely to close the deal, based on past performance. This seamless integration of data supports smoother implementation.

"Banks aren't failing to scale AI because the algorithms lack horsepower; they're failing because no one can prove the algorithms are boosting profit. Until marketing, finance and risk agree on what 'winning' looks like, AI stays stuck in pilot mode."

- Mark Owens, Managing Director, Business Consulting, Grant Thornton Advisors LLC

Ease of Implementation for Financial Institutions

Setting up a predictive lead scoring model follows a clear timeline: 1–2 weeks for preparing data, 3–4 weeks for training the model, and 5–6 weeks for deployment. To ensure the model is effective, banks need 500–1,000 historical conversions over a 12–18 month period. Before scaling, it's essential for marketing, finance, and risk teams to agree on shared KPIs, such as lifetime profit per borrower or risk-adjusted acquisition costs. Rather than trying to connect every data source immediately, banks should focus on high-impact ones like transaction history and credit utilization first.

Effectiveness in Improving Lead Prioritization

Once implemented, predictive models significantly outperform manual methods. They boast accuracy rates of 70–85%, compared to the 45–60% typically achieved by traditional systems. By relying on data instead of subjective judgment, these models eliminate biases and the influence of the "loudest voice" in sales discussions. For example, a private bank using predictive scoring for loan products achieved an 85% conversion rate by targeting the top 10–15% of leads most likely to convert. These models also act as filters, quickly flagging low-priority or non-compliant leads before they reach sales teams.

Potential ROI and Customer Acquisition Impact

Predictive lead scoring offers tangible benefits: companies using these models see 50% more leads converted while reducing acquisition costs by 33%. Businesses with well-developed scoring systems generate 192% higher revenue per email compared to those without. Sales teams also become more efficient, with productivity increasing by 33% as they focus on high-potential leads rather than wasting time on unqualified ones. To maintain accuracy, these models should be retrained every 3–6 months or refreshed automatically - Salesforce Einstein, for instance, updates every 10 days.

| Feature | Traditional Scoring | Predictive Scoring |

|---|---|---|

| Methodology | Manual rules based on assumptions | Machine learning from patterns |

| Data Points | Limited (5–10 attributes) | Extensive (hundreds or thousands) |

| Accuracy | 45–60% | 70–85% |

| Adaptability | Static; requires manual updates | Self-correcting in real-time |

4. Firmographic Lead Scoring Model

Firmographic lead scoring takes a broader view, analyzing company-level characteristics instead of just individual behaviors. By evaluating factors like industry, revenue, company size, location, and tech stack, this model helps determine how well a company aligns with your bank's Ideal Customer Profile (ICP). This approach is particularly useful in commercial banking, where the overall attributes of an organization often provide a more reliable gauge of lead quality than the engagement level of a single contact.

Relevance to Banking-Specific Needs

For banks, firmographic data is a powerful tool for segmenting leads and assigning them to the right teams. Companies can be categorized by size - such as SMBs (under 100 employees), mid-market (100–499 employees), and enterprise (500+ employees) - to ensure they are directed to the appropriate banking division. This model also acts as a risk and compliance checkpoint, automatically reducing scores or disqualifying leads from restricted industries, companies below revenue thresholds, or businesses outside your service area. Tools like Clearbit and Snowflake can fill in missing firmographic details, such as estimated revenue or business model tags, to create a fuller picture of each lead.

"Company information is vital for B2B lead scoring because it's the characteristics of a business or organization that determines lead quality rather than the individual person..." - Twilio

Ease of Implementation for Financial Institutions

Firmographic scoring is relatively simple to implement because it relies on explicit data - concrete facts that are often already in your CRM or provided directly by leads. To avoid overcomplicating the process, start with just five key firmographic variables instead of trying to analyze dozens. Reviewing past closed-won deals can help identify which traits - such as specific industries, revenue ranges, or job titles - are most likely to lead to conversions. For instance, job titles containing terms like "strategy" or "transformation" tend to have an 18% higher close rate compared to generic titles like "VP" or "Director". Regularly updating your scoring weights (quarterly, for example) ensures they stay aligned with market trends and your bank’s risk tolerance.

Effectiveness in Improving Lead Prioritization

This model is especially effective at ensuring sales teams focus on leads that align with your ICP before engaging. Automated routing systems that handle scored leads within five minutes can boost conversion rates by 20% to 40%. However, firmographic scoring has its limits when used alone - it doesn’t account for the timing of a company’s buying intent. A lead that matches your ICP perfectly may not be ready to make a purchase. That’s why successful banks often combine firmographic scoring with behavioral data to create hybrid models, ensuring they focus on leads that are both a good fit and actively interested.

"High engagement from a poor-fit lead rarely converts into revenue." - Colin Price, Head of Growth, NC Squared

Potential ROI and Customer Acquisition Impact

The returns on firmographic lead scoring can be impressive. Banks using this approach report up to a 70% increase in lead generation ROI compared to those without scoring systems. Conversion rates also see a significant boost, rising from 10% to 15–20%. By filtering out leads that don’t match your offerings or service tiers, firmographic scoring helps prevent wasted time and resources. When paired with behavioral data in a hybrid model, the results are even stronger, allowing banks to focus on leads that are both well-suited and ready to act.

5. Hybrid Lead Scoring Model

A hybrid lead scoring model merges two critical elements: fit (who the lead is) and intent (what the lead is doing). This combination provides a well-rounded view of lead quality. Instead of relying on a single data type, this model integrates demographic and behavioral insights to pinpoint prospects who align with your bank's Ideal Customer Profile (ICP) and exhibit active interest. For instance, retail banks might pair income data with online tool usage, while commercial banks could match company size with content engagement. This layered approach also incorporates negative scoring, deducting points for less desirable leads like competitors, job seekers, or individuals from non-target regions.

Relevance to Banking-Specific Needs

Banks operate in a space where they must juggle strict regulatory and credit standards with the fast-changing behaviors of digital-age customers. A hybrid model helps by balancing these demands. It assigns weight to fit factors - such as credit scores, business revenue, and geographic location - alongside behavioral indicators like visits to pricing pages, email clicks, or webinar participation. This flexibility allows banks to prioritize based on the product type. For example:

- High-value commercial loans might place more emphasis on firmographic fit.

- High-volume retail products, such as personal loans, could lean more on behavioral readiness.

This adaptable scoring system aligns with different banking needs, avoiding a rigid, one-size-fits-all solution. The tailored nature of this model also simplifies implementation, using straightforward, rules-based methods.

Ease of Implementation for Financial Institutions

The key to success here is simplicity. Start small with no more than 10 scoring factors - five for fit and five for behavior. This keeps the system manageable and easy to understand. Most banks can implement a rules-based hybrid model using data already available in their CRM, without requiring advanced AI tools. Here’s how to get started:

- Define your Ideal Customer Profile (ICP).

- Collect relevant demographic and behavioral data.

- Assign point values based on historical conversion patterns.

- Set a scoring threshold (e.g., 80+ points) for handoffs to sales teams.

- Automate the process through your CRM.

- Review and adjust quarterly.

Platforms like Salesforce or HubSpot can facilitate real-time score updates as prospects engage with your digital channels. By following these steps, banks can roll out a hybrid model quickly and effectively, without overwhelming their teams.

"A good lead scoring model is like the bouncer at a packed club - firm, fast, and focused on letting the right people through." - Hawke Media

Effectiveness in Improving Lead Prioritization

The hybrid approach addresses the blind spots often found in single-method scoring. For example, in 2024, the education platform 360 Learning paired behavioral engagement scoring with automated workload-based assignment. This resulted in 97% routing accuracy and a 40% boost in conversion rates by responding to leads within 10 minutes. Similarly, healthcare tech company Tebra implemented a hybrid scoring and routing system post-merger, achieving 40% faster response times and a 30% rise in conversion rates. For banks, this means sales teams can concentrate on leads that are not only a good fit on paper but are also ready to engage.

Potential ROI and Customer Acquisition Impact

Lead scoring delivers measurable results for banks. Studies show:

- Banks using lead scoring experience up to a 77% improvement in lead generation ROI and an 80% increase in sales productivity.

- Organizations with advanced scoring systems generate 192% higher average revenue per email compared to those without.

- Without lead scoring, conversion rates hover between 1%–6%. A hybrid model can elevate these rates to 15%–20%.

These outcomes are driven by better alignment between marketing and sales, quicker responses to high-priority leads, and reduced time spent on low-value prospects.

"Lead scoring performs best when it's tied to process (routing + SLAs) and governed as an evolving system - not a one-time rules sheet." - Pedowitz Group

Model Comparison Table

The table below highlights the strengths and considerations of the lead scoring models discussed earlier, focusing on aspects crucial to banking institutions. These include how well each model aligns with banking-specific needs, the complexity of implementation, effectiveness in improving lead quality, potential return on investment (ROI), and how it supports common banking goals.

| Model Type | Banking Relevance | Complexity of Implementation | Effectiveness | ROI Potential | Alignment with Bank Objectives |

|---|---|---|---|---|---|

| Demographic | High (Compliance/Segmenting) | Low | Moderate | Moderate | Customer Acquisition (Targeting) |

| Behavioral | High (Intent Signaling) | Moderate | High | High | Customer Acquisition (Timing) |

| Predictive | Very High (Propensity/Churn) | High | Highest | Very High | Acquisition & Retention (Churn) |

| Firmographic | High (B2B/Commercial) | Low | Moderate | Moderate | B2B Customer Acquisition |

| Hybrid | Highest (Holistic View) | Moderate to High | Very High | Very High | Overall Efficiency and Growth |

Key Takeaways:

- Demographic and Firmographic Models: These are well-suited for banks focusing on compliance or clear customer segmentation. However, they primarily identify who the lead is without offering much insight into their readiness to act.

- Behavioral Scoring: This model excels in tracking intent signals, such as interactions with a mortgage calculator or downloading loan guides. Such signals are critical for "speed-to-lead" scenarios, where timing is everything.

- Predictive Models: These deliver top-tier effectiveness and ROI, particularly for retention strategies like predicting customer churn. They leverage advanced data analytics to anticipate future behaviors.

- Hybrid Models: Combining fit, behavior, and intent into a single operational score, hybrid models provide a comprehensive view. As The Pedowitz Group explains:

"High-performing teams use a hybrid model that combines fit + behavior + intent and then calibrates it to pipeline conversion and sales capacity"

Ultimately, the best model for your bank depends on your data infrastructure, team expertise, and strategic goals. Each model has its unique advantages, allowing institutions to tailor their approach to meet specific needs effectively.

Conclusion

Lead scoring models are reshaping how banks approach customer acquisition and engagement by zeroing in on prospects with the highest intent. By categorizing leads into hot, warm, and cold groups, these models enable banks to tailor their outreach, leading to measurable boosts in ROI and efficiency.

The adoption of predictive analytics and AI-driven models takes this a step further, helping banks uncover ready-to-buy customers by detecting patterns that traditional methods might miss. As Mark Owens, Managing Director at Grant Thornton, points out:

"Banks aren't failing to scale AI because the algorithms lack horsepower; they're failing because no one can prove the algorithms are boosting profit".

However, success doesn’t come without challenges. For these models to deliver results, banks need alignment across marketing, finance, and risk departments, ensuring everyone agrees on what defines a qualified lead and how to measure success. Yet, implementation hurdles remain significant.

Integrating lead scoring systems is no small feat. Banks often grapple with fragmented data, managing decaying scores for inactive leads, and building effective trigger-based workflows. In fact, nearly 40% of banks report data quality issues as a major obstacle.

Strategic partnerships can make all the difference here. Collaborating with experts like SEO Werkz can help banks navigate these complexities. From integrating marketing automation tools to defining precise MQL-to-SQL criteria and establishing closed-loop reporting, professional support ensures that marketing efforts directly tie back to revenue. Trigger-based workflows, for instance, have proven to achieve 8x higher open rates compared to standard campaigns, turning potential challenges into opportunities for growth.

Whether your bank opts for demographic, behavioral, predictive, firmographic, or hybrid models, the goal remains the same: aligning sales efforts with the most promising prospects. By choosing a model that fits your data capabilities and strategic objectives, you can focus your resources where they’ll have the greatest impact. In today’s competitive environment, that’s a game-changer.

FAQs

Which lead scoring model should my bank start with?

The ideal lead scoring model for your bank should pinpoint what qualifies a lead as "sales-ready" by emphasizing timing, intent, and fit. To do this, leverage both demographic and behavioral data to identify and prioritize leads with the highest likelihood of converting. By combining engagement metrics with fit criteria, you can help your sales team zero in on the most promising prospects efficiently.

What data do we need to build a predictive lead scoring model?

To build a predictive lead scoring model, start by collecting demographic data like industry, company size, location, and growth stage. This helps determine how well a lead aligns with your ideal customer profile. Next, gather behavioral data, such as website visits, email opens, and content interactions, to gauge their level of interest. By blending these two types of information, you can better understand which leads are most sales-ready, making it easier to prioritize efforts and boost conversion rates.

How do we set an MQL score threshold and route leads to sales?

To establish an MQL score threshold, start by determining what makes a lead "sales-ready" based on their fit and level of engagement. Assign a specific score range, such as 60–80 points, within your CRM or marketing automation platform. Then, set up routing rules to ensure leads exceeding this score are automatically passed to your sales team. Make it a habit to review and tweak the threshold regularly, using conversion rates and feedback from sales to fine-tune the process for better results.